The Token Trap

"I want to believe"

Today I take a break from our regularly-scheduled AI programming to devote some time to crypto – an industry I hold dear and in which I have been deeply involved since its inception, but one that I’ve increasingly distanced myself from since starting Nazaré Ventures. As Mulder in the X Files often says “I want to believe” (but I’m still looking for aliens).

As I wrote in my earliest Nazaré blog post:

“My journey in AI began in 1993 when I started a PhD researching neural networks for speech recognition. I was fascinated by the idea of creating a machine that could think and help us with our lives… In 2000 I moved on from AI after realizing that the majority of the industry was focused on “mining humans” through the use of ad tech. My work with Orchid Labs has been an attempt to counter the rise of surveillance capitalism, often powered by AI models.

For the last 11 years I’ve been focused on investing in and building companies focused on decentralized technologies, starting with Bitcoin in 2013 at Pantera Capital and then Ethereum with Orchid Labs in 2017 and many more over the last few years as an angel investor.

In 2020 I began to notice some early signs of hope in the use of AI for different purposes. The world of AI had suddenly become exciting again and I became fascinated. Earlier [in 2023] I started a new fund to focus on AI.

Nazaré Ventures represents a culmination of my work since 2013, combined with my original studies in AI.”

A Tale of Two Cities

In thinking about this piece, Dicken’s iconic opening line in a Tale of Two Cities feels to me like an apt description of where I stand with respect to AI and crypto.

“It was the best of times, it was the worst of times.”

If you’re a regular reader, you’re familiar with the extraordinary advances happening in artificial intelligence. Despite what I believe to be inflated financial valuations, I have written extensively about how promising AI is, and how exciting it is to be so deeply entrenched in the industry. It is very clearly “the best of times” when it comes to AI.

On the other hand, if you happen to follow crypto, you’re probably familiar with the catastrophic crash in token prices – including the majors like BTC, ETH, and SOL – that happened around October 10 of last year, along with the overwhelmingly negative sentiment permeating the industry and the news coverage since then. Despite a favorable regulatory environment, a pro-Bitcoin POTUS, and traditional finance finally accepting that DeFi is the future, it is yet again “the worst of times” for crypto and its tokens.

In fact, the tokens are precisely what I’d like to explore in today’s essay.

I’ve been thinking deeply about the following question, which I’ll attempt to answer below: Why do crypto tokens fail as a funding and product mechanism – and what should the industry do instead?

Decentralization

We must first start with decentralization. Yes, it’s real, and yes, it’s useful. As centralized entities gain power, wealth, and influence, they tend to increase their gravitational pull, concentrating their position and exerting more control over the rest of their ecosystem. This can be true in private enterprise, local/state/national governments, and nearly all organizations that involve humans (and now even machines).

Forces that act to counter-balance the natural tendency to concentrate power and influence are healthy, and deserve to be pursued both on principle – say, for example, as open-source, non-profit, or NGO initiatives – and even as profitable endeavors if they can survive.

Bitcoin is the most obvious crypto-native example. Distributed ledgers route around centralized banking and the sometimes oppressive world of traditional finance. Peer-to-peer exchange of financial value is a real innovation that deserves to exist, and the mathematics and cryptographic primitives introduced by Bitcoin are intrinsically valuable on their own.

Ethereum, another brilliant innovation, built on the Bitcoin principles and created other important primitives: smart contracts, computers that can make commitments, and – critically for the rest of the industry – a way to launch one’s own token. As such, ETH created the “World Computer” to which everyone could contribute, and found a way to route around centralized fundraising.

But we all know what happened next.

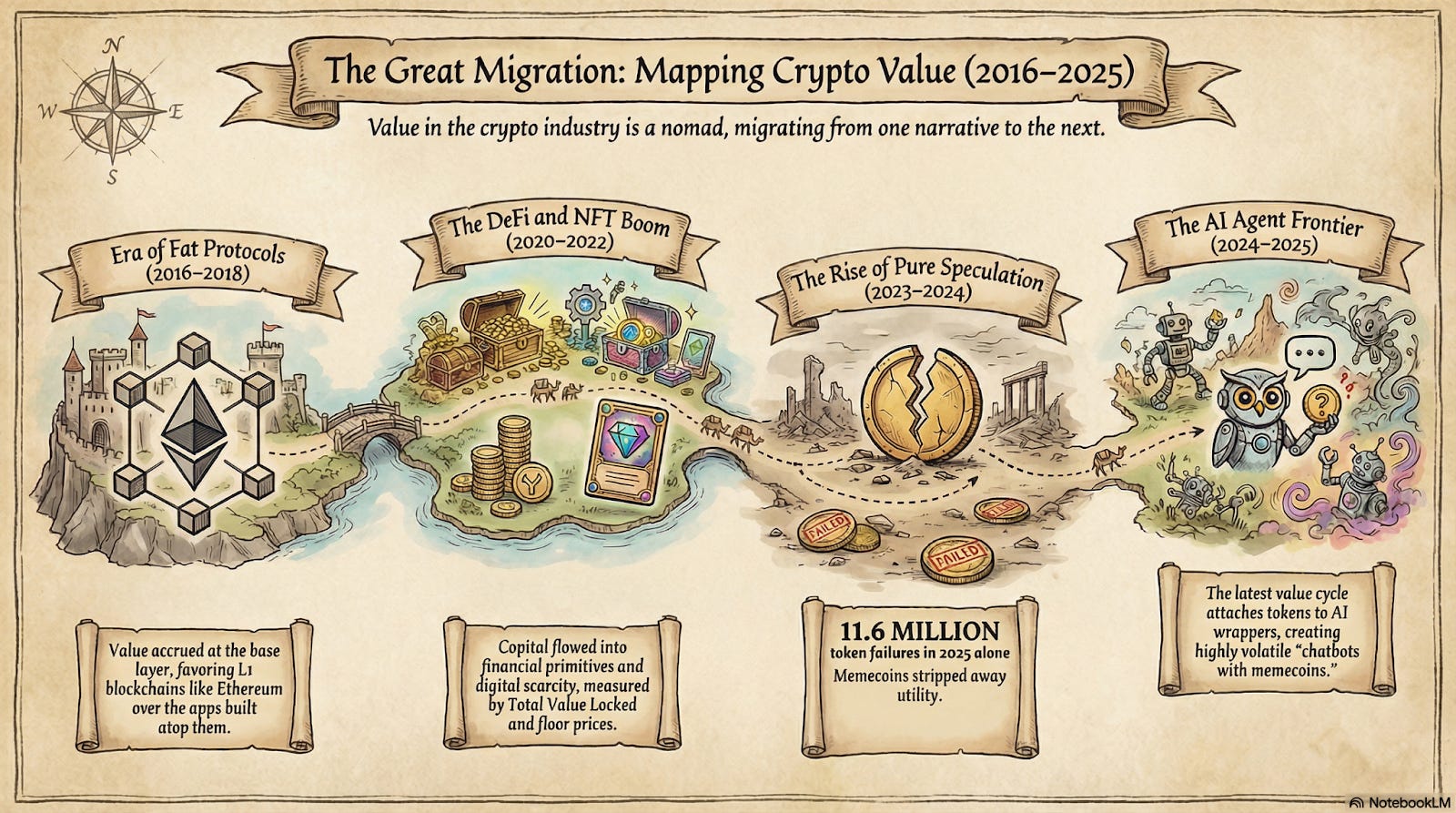

In short order came the ICO boom, and the speculative boom-and-bust token cycles for which crypto has become notorious were born.

The truth is that decentralized protocols, no matter their importance on principle, are not always companies that should operate as for-profit entities that merit venture capital investment. In fact, the vast majority simply are not (see current token prices).

Lorenzo Valente (Ark Invest)

Somewhere along the way, decentralization became a meme. It became a shield, of sorts, behind which every “project” hid as an excuse for its lack of product-market-fit, and it gave the entire industry cover to continue funding, building, and “bringing to market” (read: launching tokens) things nobody used.

In the beginning “Maxis” were spawned for every major coin, relentlessly faithful to their “one chain to rule them all” and extraordinarily active and vocal on crypto twitter. Questioning the project, product, or core developer team meant questioning the cause and was grounds for public excoriation.

But after all the breathless twitter infighting and money that’s been won (but mostly lost), what do we have to show for the last ~15 years? Bitcoin, ETH and DeFi have emerged as victorious (although maxis are disappointed because BTC has been co-opted by tradfi, fears about quantum abound, and ETH price action has been flat out abysmal), but the rest is a graveyard. Altcoins are an unmitigated disaster, and everything related to “crypto x AI” is little more than vaporware – especially the crypto x ai tokens.

So here we stand. We’ve got institutions on board, regulations out the way, technology that scales – we’ve simply run out of excuses. We are like teenagers yelling to our parents that we want more, even though we got everything we wanted. Everything’s aligned, but there’s an elephant in the room we haven’t named: nobody’s building proper startups. Ones that look at product-market fit and actually try to adjust. Forget infra, forget regulation, forget token prices. Nobody’s building actual companies or enduring businesses.

One Instrument Doing Too Many Things

One token is simultaneously:

Capital raise (ICO, TGE, SAFT -- however you dress it up)

Governance (voting, proposals)

Utility (pay for the service, access the network)

Equity (people buy it as ownership, whatever the legal wrapper says)

Incentive (airdrops, staking rewards, emissions)

No financial instrument has ever done all five at once. How do you price it? By revenue? By users? By governance votes? You can’t. That’s in part why the Blockworks Token Transparency Framework exists -- 30+ protocols needed a third party to build basic disclosure standards, because the conflation makes valuation impossible and increases the temptation to grift, rugpull, or commit fraud.

Your equity holders want the price up. Your users need the price down to afford the service. Those two forces constantly and incessantly fight each other inside the same instrument.

ETH gets away with it (and even for ETH the price action isn’t great…). Gas plus security plus store of value -- those functions reinforce each other by design. But most projects aren’t Ethereum. Most projects copied the token model by default for lack of a better idea (or deliberately to secure early liquidity). The end result, more often than not, is a meme coin with a few PhDs attached.

Crypto is Technology & We Built Backwards

Here’s the honest truth: crypto is technology.

Technology (usually) has one rule that simply cannot be ignored – it must be useful to be valuable.

There were bad ideas on the internet, bad ideas on mobile, bad ideas in the cloud, and bad ideas in crypto. Every technological revolution or paradigm shift has failures – that’s how innovation works! You build, you find out nobody wants what you’ve built, you kill it, you move on, you adapt, or you fail.

But in crypto, the ones without product-market fit didn’t die. Crypto had two precious elements that permitted the industry to subvert this rule for more than a decade: decentralization and tokens. Because we used decentralization as ideological cover and we had instant liquidity through tokens, we funded, built, and monetized based on memetics, narratives, and vibes.

Crypto even invented its own metrics to avoid this reckoning. Ideas got funded to the tune of tens and sometimes hundreds of millions of dollars based on a whitepaper. That money was then used to fund “incentives” designed to boost certain activity metrics in an effort to demonstrate adoption, usage, and utility. TVL. Token holders. Governance participation. Discord members. These let projects look successful without anyone actually using the product.

For what it’s worth, I lived through this exact script once before. In 1998, you raised on a PowerPoint (early version of a whitepaper), bought Yahoo traffic (like wash trading or incentive-boosted metrics), and went public fast on thin markets (like launching a token).

And then came the airdrops… Of the airdrops! Free money! Quite literally, free money out of thin air.

In fact, in a recent article titled “The Future of Token Launches,” Legion writes about airdrops: “The dominant distribution mechanic of the last cycle put tokens in wallets at zero cost basis, then priced the asset as if those wallets were investors. Recipients with a rational expectation of price decline do the rational thing. They sell. And they sell aggressively. Nobody should have been surprised by what happened next, and yet, every cycle, people are.”

For “yield farmers” and “airdrop hunters” during DeFi summer, this was an exceptionally lucrative time to be active onchain. But if you didn’t get out before FTX, it didn’t matter anyway.

It didn’t get better over time, either. According to the same Legion article, 28 tokens launched above $1B FDV (Fully Diluted Valuation) between 2023-2025. None ever traded above listing price. 85% of tokens launched in 2025 ended the year negative. The median return? - 69%.

Prices simply went straight down, and in the same year that Bitcoin hit all-time highs! The tide rose! The industry was supposed to have won! But the narratives had run out, and most of the boats sank anyway.

We built backwards, financializing before we had product-market-fit, and in so doing the token – and specifically the token’s price – became the product.

What surprised me was everyone else. How liberated people feel when you say it out loud. They’ve come up after talks and in general conversation (“thank you so much for saying this!”) as if they needed permission to agree with what they already knew was true.

The Migration

The talent knows it too. The most talented founders of our generation were with us in the beginning. Many of them built on Ethereum, contributed to the ecosystem, and believed in the vision. Now they’ve all left for AI.

They left because crypto companies with tokens are toxic and can’t be acquired because traditional companies won’t touch tokens. Top talent gets stuck in speculation cycles with no clean exit. They left because DeFi is still running a 2017 mental model while AI moves at light speed. They left because crypto consumer products are nearly impossible to fund now (do they even exist?), and the people who would have built them are building AI companies instead. All the capital and all the talent is flowing the same direction.

In my experience, founders love building things people use. They love that more than they love making money. And unfortunately, nobody’s using crypto much at all.

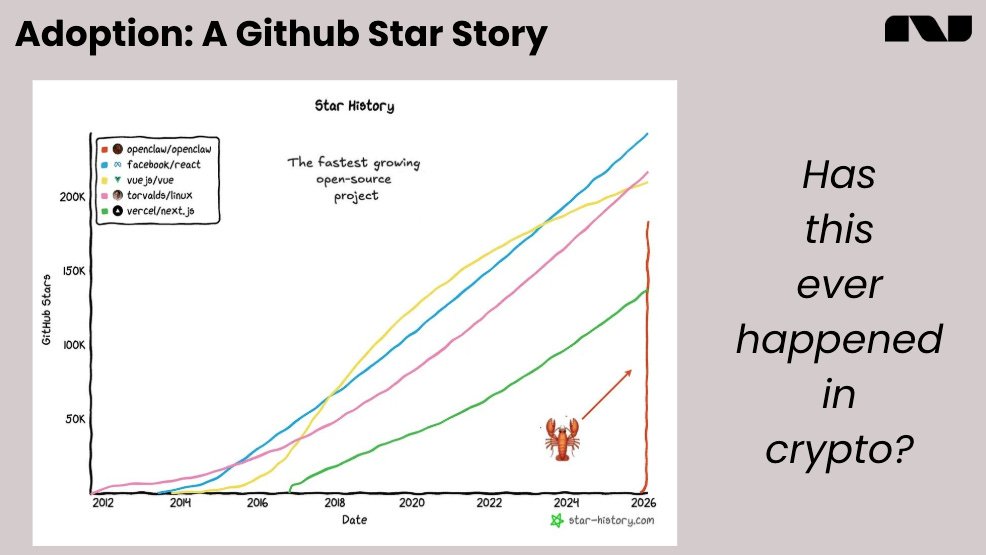

A particularly salient example of this and the utility function can be found in OpenClaw, the most popular (and powerful) current autonomous agent framework developed as an open-source initiative by Austrian developer Peter Steinberger. (We wrote about OpenClaw here)

OpenClaw is the fastest growing open-source project in history, and by a wide margin. Now, even if we ignore the incentives that drove most of the onchain activity, has an application in crypto ever seen this much adoption? The answer is categorically no, and therein lies the rub.

The Remedy

I helped shepherd the first real Bitcoin investment vehicle. I was there for the birth of Ethereum and built on the network early. I deployed capital into this ecosystem before most people reading this had heard of it.

BTC, stablecoins, DeFi, tokenization, prediction markets, 24/7 casino and hyper-financialization – those are the ideas that are working. People use them, and they solve something real, even if what they sometimes solve for is the universal human desire to gamble at three in the morning (otherwise known as “Long Degeneracy”). That’s where the next decade gets built – everything else is a curiosity at this point.

I was seed in Circle, and they IPO’d with pure equity. I was seed in Abra, now going public via SPAC – equity again. Token for the stablecoin, equity for the company. The two most successful crypto companies I ever backed both chose the instrument that matched the job. That should tell you something.

I built Orchid because I believed in decentralization. I believe in it more now, not less. As a society, we need it. But we keep trying to mix cypherpunk with money, and money wins every time. The tool eventually becomes the product, the mission becomes the narrative, and the “community” becomes the cap table. That combination is not, unfortunately, a winning formula.

Now, maybe the answer was never venture-scale token businesses. Maybe that was a mistake, and the answer was always fair launches, proof of work, open source. Bitcoin showed us that much – no pre-mine, no VC round, no foundation with a war chest.

We can call our industry “crypto,” and we have the right to be proud of what it is. But we should stop trying to make it what it’s not, or trying to be something else entirely.

Because crypto is ultimately finance with better engineering, full stop. Every time the industry reaches outside financial services, we make the thing it’s actually good at look silly (or worse…criminal). The truth is the boring stuff won, and that’s ok. Stablecoins settled $33 trillion last year; banks are coming onchain; tokenization is real. That’s the whole game, so put your suit on, roll your sleeves up, and build the future of finance.

If you’re building in crypto, act like what you are: a tech founder who happens to use these tools. Find a problem, build a solution for real users, get to revenue. Token later…if ever. And if you’re investing, stop funding memes, vibes, and narratives. Fund products people use without being paid to use them.

That’s all I’m asking for. I’ve spent a decade on this. I want protocols that run because they’re useful, not because someone’s bag depends on it. People, companies, and products that outlast the speculation.

Steven Waterhouse

General Partner, Nazaré Ventures